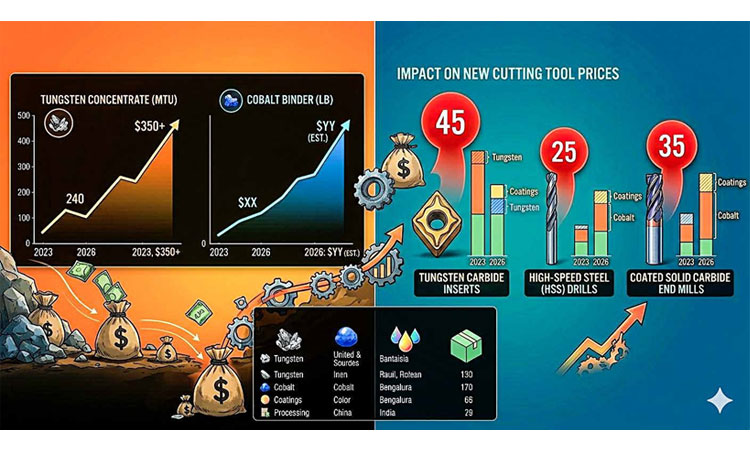

As of early 2026, the global tungsten market has reached a fever pitch. With prices for tungsten concentrate breaching the $350 per mtu (metric ton unit) mark—a staggering 45% increase over the last 36 months—the Indian machining industry finds itself at a crossroads. For a sector where cutting tools typically account for 3% to 5% of total production costs, these inflationary pressures are no longer a background noise; they are a threat to the bottom line of every MSME and industrial giant in the country.

However, hidden within this “Carbide Crunch” is a powerful opportunity that could redefine India’s manufacturing resilience. The raw material India needs isn’t buried in a distant mine; it is sitting on the shop floors of its own factories in the form of scrap.

The Anatomy Of The Crisis: Imports And Geopolitics

India’s vulnerability stems from a heavy reliance on external sources. Currently, the nation imports nearly 80% of its tungsten requirements. This dependency is particularly precarious given the concentration of global supply. China, which controls approximately 82% of global primary tungsten production, has systematically tightened export quotas to prioritize its own burgeoning high-tech and EV sectors.

Furthermore, the “cement” in cemented carbide is Cobalt, a mineral whose price is tethered to the volatile battery market. As India scales its own EV targets for 2030, the cutting tool industry is effectively competing with gigafactories for the same expensive ore.

The math is becoming untenable. A standard carbide insert that cost a few hundred rupees three years ago has seen its cost basis shift dramatically. For Indian manufacturers to remain competitive on the global stage, the “use-and- throw” model of tooling must be replaced by a high-velocity circular economy.

In the high-precision corridors of Indian manufacturing—where the sparks of aerospace components, automotive gears, and defense hardware fly daily—a quiet crisis is unfolding. It isn’t a lack of order books or a shortage of skilled labor. It is the skyrocketing cost of the very “teeth” of the industry: Tungsten Carbide.

Mining The Factory Floor: The Value In The Waste

Carbide scrap—often referred to as “Black Gold” by those in the know—is arguably the most valuable waste stream in a machine shop. Unlike many other industrial byproducts, tungsten carbide is infinitely recyclable without significant degradation of its mechanical properties.

The benefits of pivoting to a formal recycling infrastructure are backed by compelling figures:

- Energy Arbitrage: Producing 1kg of tungsten from recycled scrap consumes 70% less energy than extracting it from virgin ore. In an era of rising power costs and carbon taxes, this is a massive operational advantage.

- Carbon Footprint: Recycled carbide generates approximately 40% less $CO_2$ emissions, aligning perfectly with India’s “Green Manufacturing” mandates.

- Yield Efficiency: Modern Zinc Process recycling can recover up to 98% of the cobalt and tungsten from used tools. This isn’t “downcycling”; it is the creation of near-virgin grade powder that can be pressed into new, high-performance tools.

- Economic Impact: If India were to organize its fragmented scrap market, the industry could potentially save over $150 million annually in procurement costs by 2028.

The Infrastructure Gap: Bridging The Informal Divide

Despite the obvious economics, India’s recycling landscape remains dangerously fragmented. Currently, it is estimated that over 60% of India’s carbide scrap leaks into the informal sector. Here, it is often sold for quick cash to traders who export it as low-value waste or process it in rudimentary facilities that suffer from high contamination and poor recovery rates.

To capture this value, India needs a National Carbide Recovery Grid built on three pillars:

Technology-Driven Collection (The Digital Loop)

The primary challenge is not the recycling itself, but the collection. Thousands of small workshops treat spent inserts as floor sweepings. By implementing Digital Tool Management and blockchain-verified scrap tracking, large OEMs can ensure that every gram of carbide sold eventually finds its way back to a certified recycler. This turns scrap from a “waste disposal” problem into “working capital.”

Specialized Recycling Clusters

Recycling carbide is a sophisticated chemical and metallurgical process. India requires specialized clusters in hubs like Pune, Bengaluru, Chennai, and Ludhiana. These clusters should house two primary technologies:

- The Zinc Process: A physical recycling method where molten zinc makes the carbide “swell” and crumble into a powder. It is cost- effective and ideal for high-quality scrap.

- Chemical Reclamation: A more intensive process that breaks the tool down to its atomic components (Tungsten Acid and Cobalt Salt), allowing for the removal of all contaminants and coatings.

Policy And Fiscal “Nudges”

The government’s National Critical Mineral Mission (2025) has laid the groundwork, but more is needed. A reduced GST rate for certified recycled carbide powder, or “Recycling Credits” similar to carbon credits, could incentivize MSMEs to bypass the informal “cash” market in favor of organized channels.

A Call For Collective Action

No single company can solve the carbide crunch in isolation. It requires a “Triple Helix” collaboration between industry, academia, and government.

- Industry Associations: Bodies like ICTMA ( Indian Cutting Tools Manufacturers Association ), IMTMA (Indian Machine Tool Manufacturers’ Association) must lead awareness campaigns to educate shop owners that their scrap bucket is actually a secondary bank account.

- Tool Manufacturers: Global giants and domestic players alike must expand Buy-Back Programs. By offering credits toward new tools in exchange for old ones, they secure their own raw material pipeline while lowering the customer’s TCO (Total Cost of Ownership).

- Large OEMs: Companies in the automotive and aerospace sectors should mandate “Recycled Content” percentages in their tooling tenders, forcing the supply chain to adopt circular practices.

The Competitive Edge: Resource Intelligence

The next decade of manufacturing will not be won just by those with the fastest spindle speeds

or the cleverest tool paths. It will be won by those who exhibit Resource Intelligence.

In a world where mineral scarcity is the new normal, a robust recycling infrastructure is India’s “Secret Weapon.” It reduces dependency on volatile foreign markets, slashes energy consumption, and provides a buffer against geopolitical shocks.

The “Carbide Crunch” is more than a cost headache; it is a turning point. If India can transform its scattered scrap into a national resource pool, it won’t just be saving money—it will be securing its industrial future. The goal is clear: by 2030, a drill bit used in a Chennai factory should be reborn as a milling cutter in a Pune plant, over and over again. That is the true meaning of a self-reliant, “Atmanirbhar” manufacturing sector.