China has increasingly weaponized its dominance over critical commodities and rare earth materials by controlling large portions of global mining, processing, and export supply chains. Through export restrictions, production quotas, and preferential allocation to domestic industries, strategic raw materials such as rare earths and tungsten have been transformed from freely traded commodities into instruments of industrial leverage. This approach has distorted global markets, driven sharp price increases, and compelled importing countries to rely on Chinese finished products rather than just raw materials. For India, this concentration of supply exposes serious vulnerabilities in key manufacturing sectors and underscores the urgent need for strategic mineral security, supply diversification, and domestic processing capabilities.

The current situation is not merely a cyclical commodity fluctuation but reflects a deliberate and long-term strategic approach adopted by the world’s second-largest economy. China produces over 80% of global tungsten supply and controls a substantial share of global reserves, positioning it as the dominant force in the tungsten value chain. Beyond mining, China has systematically moved downstream, from raw ore to ammonium paratungstate (APT), tungsten powders, carbide blanks, and finally finished cutting tools.

By restricting exports of APT and tungsten carbide, China has effectively:

- Prioritized domestic manufacturers

- Strengthened its advanced manufacturing ecosystem

- Forced global buyers to increasingly source finished Chinese carbide tools instead of raw materials

- Enhanced its strategic leverage in defence, aerospace, and high-precision manufacturing sectors

This shift has transformed China from a raw material supplier into a global price-setter and industrial gatekeeper.

Key Challenges for Indian Carbide Tool Manufacturers

- Rising Input Costs : Indian carbide tool producers face sharply higher raw material import costs, compounded by currency volatility and reduced price competitiveness against Chinese and Korean competitors.

- Margin Compression : Small and mid-sized Indian toolmakers, already operating on thin margins, struggle to pass on rising costs to price-sensitive customers, particularly in automotive and MSME manufacturing.

- Supply Risk and Lead-Time Volatility : China’s export restrictions have increased procurement uncertainty, forcing Indian firms to hold larger inventories, pay spot-market premiums, and seek alternative suppliers with inconsistent quality and reliability.

- Competitive Threat from Chinese Finished Tools : As China increasingly channels tungsten into finished tool exports, Indian manufacturers risk being undercut by competitively priced Chinese carbide tools, threatening domestic production capacity and employment.

Strategic Responses: What Indian Cutting Tool Makers Can Do

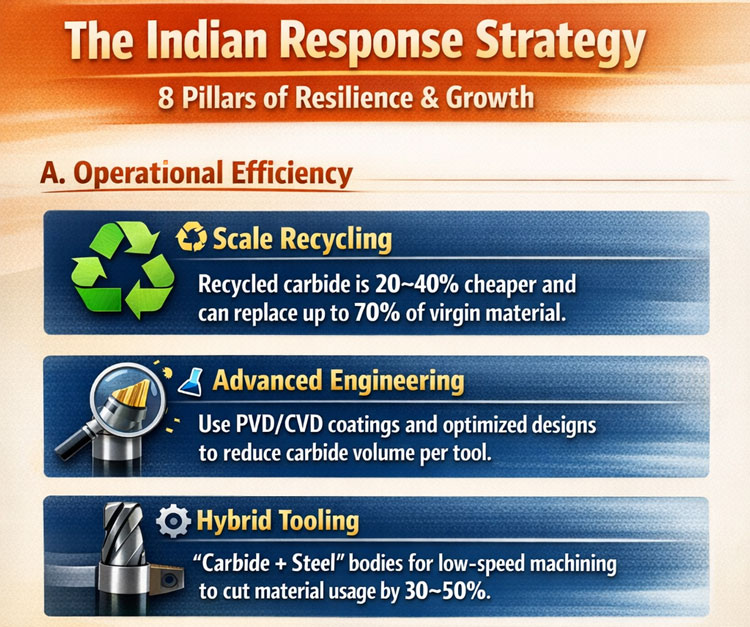

1. Scale Tungsten Carbide Recycling

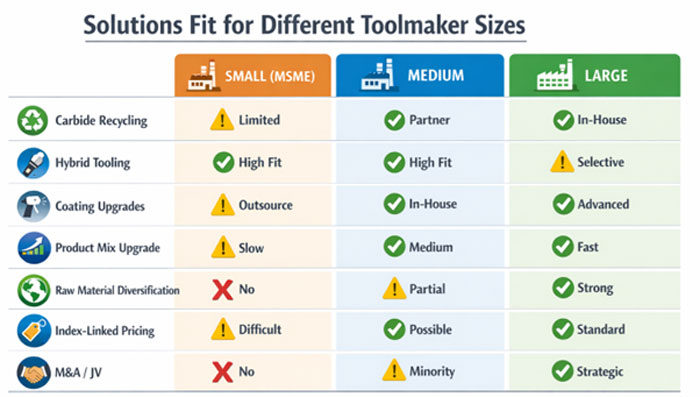

Recycled carbide can replace 30–70% of virgin tungsten in many tool grades at 20–40% lower cost. Indian manufacturers should establish scrap buy-back programs with customers and partner with global carbide recyclers in Europe and Japan while developing closed-loop recycling models with automotive and aerospace OEMs. Recycled carbide can be effectively deployed in general machining grades, mining and wear parts, and non-aerospace applications.

Industry bodies such as IMTMA and ICTMA should actively seek government incentives for carbide recycling under critical minerals and circular economy initiatives.

2. Reduce Carbide Consumption per Tool

Improved tool design, optimized substrates, and advanced PVD and CVD coatings allow manufacturers to achieve longer tool life with lower carbide consumption per component. While this may reduce demand for low-cost commodity tools, the strategic shift must be toward cost-per-part pricing rather than tool price. The focus should be on selling performance, not raw material content.

3. Hybrid Tooling: Carbide + Steel or HSS

Significant carbide reduction is possible in drills, reamers, and form tools used in low-to-medium speed machining, particularly for MSME and job-shop customers. Hybrid tooling solutions can reduce carbide usage by 30–50%, improve price acceptance, and lower exposure to tungsten price volatility.

4. Move Up the Value Chain

Indian toolmakers must increasingly focus on segments that require high-performance carbide solutions and have greater pricing resilience. These include aerospace and defence machining, EV motors and battery components, railways and heavy engineering, and oil & gas or power generation. In such applications, raw material cost forms a smaller proportion of the selling price, while customer lock-in and value addition are significantly higher.

5. Diversify Raw Material Sourcing to Reduce China Dependence

Alternative sourcing from Vietnam, Korea, Rwanda, and Bolivia must be actively pursued. Free trade agreements with ASEAN and Korea, along with recent trade arrangements with Europe and the United States, open up multiple sourcing opportunities. An industry-level pooled procurement model, potentially facilitated by ICTMA, could further enhance bargaining power. Even partial diversification materially improves supply security.

6. Long-Term Pricing and Customer Contracts

Larger toolmakers should introduce raw-material index-linked pricing and price-variation clauses similar to those used in steel contracts. In return, customers can be offered tool management programs, annual tooling contracts, or vendor-managed inventory models. The objective is to share volatility rather than absorb it entirely.

7. Government and Industry-Level Interventions

Tungsten and carbide must be formally classified as critical materials. Taking cues from the recently announced Rare Earth Corridor Policy (Budget 2026), targeted incentives should be extended to carbide powder manufacturing, recycling plants, and coating technologies. Import duty rationalization on APT, tungsten powder, and coating equipment is essential. Industry bodies such as CII, IMTMA, and ICTMA should establish common testing and coating centres, shared recycling infrastructure, and coordinated global sourcing partnerships.

8. Strategic M&A and Joint Ventures

Mid-to-large toolmakers should actively explore acquisitions of recycling companies in India or overseas, as well as technology partnerships or joint ventures with European powder producers and coating technology firms. Accelerated backward integration into scrap processing and powder blending at scale is critical to permanently reducing cost volatility.

Conclusion

For Indian cutting tool manufacturers, waiting for tungsten carbide prices to normalize is not a strategy. The winners in this environment will be those who use less carbide, recycle more, sell performance rather than material, and decisively move up the value chain. Higher value addition must increasingly happen in India if the domestic tooling industry is to remain competitive, resilient, and strategically relevant.